Every month our research team looks into the climate tech news, deals, and trends shaping the industry. In April, we saw the G7 taking a unanimous decision to shut down all coal plants within the next decade, private equity firms raising billion-dollar climate funds, and a slew of interesting activity within climate tech. Here are the latest updates on the state of climate tech.

- Capital injection slows but exit activity sees an uptickFunding activity for April dipped by 20% compared to the previous month, and by 22% compared to this point in 2023. Compared to investment activity from January till March, April has recorded the least amount of funding and deals, suggesting that the mega-round frenzy that characterized the start of 2024 might be tapering off.However, even though investors within climate tech are cautious about the volumes of capital they inject into ventures within the space, liquidity activity saw a noticeable uptick in April. What’s more, all the exits that occurred in April were acquisitions. More specifically, 40% of these acquisitions were software solutions, while the remaining 60% were hardware solutions.

- Average mega-round deal tickets shrink in AprilFrom January to March, the average mega-round ticket size was between $613m and $411m, with notable inclusions of giga-rounds across each of the three months. However, April’s average hovered around $170m, with the highest mega round ticket beingNexamp’s $520m growth equity investment.

This shrinkage is a consequence of muted debt activity across all regions, most especially within Europe where debt funding for April shrunk by 85% MoM and almost 100% compared to January’s $10.3b debt funding record.

Climate tech funding: Last month’s patterns

Within the last 30 days, there has been a recorded $4.83b in funding across 350 deals. The funding split was skewed significantly to dilutive funding, with the 211 equity deals securing 84% of total funding, while non-dilutive deals comprised the remaining 16% (with debt comprising almost 90% of total non-dilutive funding). Most of the large ticket deals that happened in the last 30 days were mainly equity deals within energy and transport. Most notably were Pinegate Renewables’ $650m and Nexamp’s $520m growth equity rounds, both of which targeted growth and expansion plans, as well as the acceleration of capacity to meet growing market and customer demand for renewable energy in the US and beyond.

Shifting the lens to a capital stage focus, we see pre-seed and seed funding and deal numbers decline by 22% and 39% respectively MoM, but still on par with the three-month rolling average for the months in Q1 2024. The same funding and deal MoM decline story persists for early stage companies, with these companies declining by 48% and 26% respectively. The later stage segment was the only segment to see relative resilience in funding and deal numbers for the month of April, recording $2.45b in funding across 36 deals; a 167% funding growth and 30% deal growth MoM. Notable deals that occurred within this segment are (asides the PineGate and Nexamp deals) Stellantis’ $100m backing of 360 energy, Tes Energy’s $150m Series C round, and Platform Science’s $125m Series D round.

Shifting the lens to a capital stage focus, we see pre-seed and seed funding and deal numbers decline by 22% and 39% respectively MoM, but still on par with the three-month rolling average for the months in Q1 2024. The same funding and deal MoM decline story persists for early stage companies, with these companies declining by 48% and 26% respectively. The later stage segment was the only segment to see relative resilience in funding and deal numbers for the month of April, recording $2.45b in funding across 36 deals; a 167% funding growth and 30% deal growth MoM. Notable deals that occurred within this segment are (asides the PineGate and Nexamp deals) Stellantis’ $100m backing of 360 energy, Tes Energy’s $150m Series C round, and Platform Science’s $125m Series D round.

Climate tech patterns: A shift in investment focus from early to late-stage

One of the most obvious patterns exhibited in April has been on display from the tail end of 2022 into 2023: the snail-place shift in investor focus from the very early stage to the late stage. Could this shift continue to be indicative of maturation within climate tech? It’s too early to say. Nevertheless, this pattern clearly shows that early-stage innovations that received investment post the years of climate tech1.0 (and maybe just pre-pandemic) are beginning to bear fruit, attracting greater interest and investment as they progress along the development pipeline. As these companies advance from ideation to implementation, they become increasingly attractive to investors seeking both financial returns and environmental impact, prompting a realignment of investment strategies towards later-stage opportunities.

Examining the different regions reveals distinct trends in venture funding dynamics for climate tech. North America, particularly the US, maintains a steady anchor in venture funding, hovering around $2.0b. However, in Europe, the enthusiasm surrounding debt funding appears to be waning, as April saw just over $200 million in debt funding, contributing to a lackluster funding landscape for the region during the month. This is against the backdrop of large debt-structured rounds within the region in the first three months of 2024, leaving questions about whether the debt hype has been culled for now. But of course, we’ll need to examine the coming quarters to truly get the bigger picture. Notably, the only regions to experience positive month-over-month funding growth were South America and Oceania.

And potential implications? The resilience of North America’s venture funding ecosystem continues to reinforce its status as a global innovation powerhouse, with ample, ready-to-be-deployed capital available to fuel venture growth. Conversely, while too early to say, Europe’s seeming slowdown in debt funding may signal a need for recalibration in funding strategies or a shift in investor sentiment towards alternative forms of financing. There’s also a point to be made that April was perhaps a very quiet month. The positive funding growth in South America and Oceania could be a marker for emerging opportunities in these regions, potentially attracting greater investor attention and fostering the development of vibrant startup ecosystems. However, the concentration of exit activities in North America and Europe underscores the dominance of these regions in terms of mature, acquisition-ready startups, highlighting the challenges faced by emerging markets in achieving similar levels of exit activity and investor liquidity.

Climate tech surprises: Investor syndications taking form

With surprises, the point is to highlight some specific observation that either deviates from a defined pattern or erupts as a new realization for the research team. We analyzed our proprietary investor data and observed something curious: there are clear syndication or consortia patterns amongst some of the main investor groups.

In fact, for the deals that we observed over the past 30 days, 36.2% of them had some form of investor syndication, i.e. over a third of the deals had multiple investor combinations participating, while the remaining 64% of them were participated solely by one investor group. This observation could be indicative of several implications, some of which could include de-risking opportunities, increased deal competition, network/expertise leveraging, and enhanced due diligence capabilities.

But what are the most common of the consortia groups (are VCs and Corporate investors combining much more than Growth Equity and Banks for instance)? How do they compare over the previous years? What types of deals feature the most consortia? And what could this mean for climate tech in the coming months?

The Market Insights team at Net Zero Insights remains vigilant in monitoring the progression of this indicator and will be sure to furnish additional updates in our forthcoming research publications focused on the State of Climate Tech.

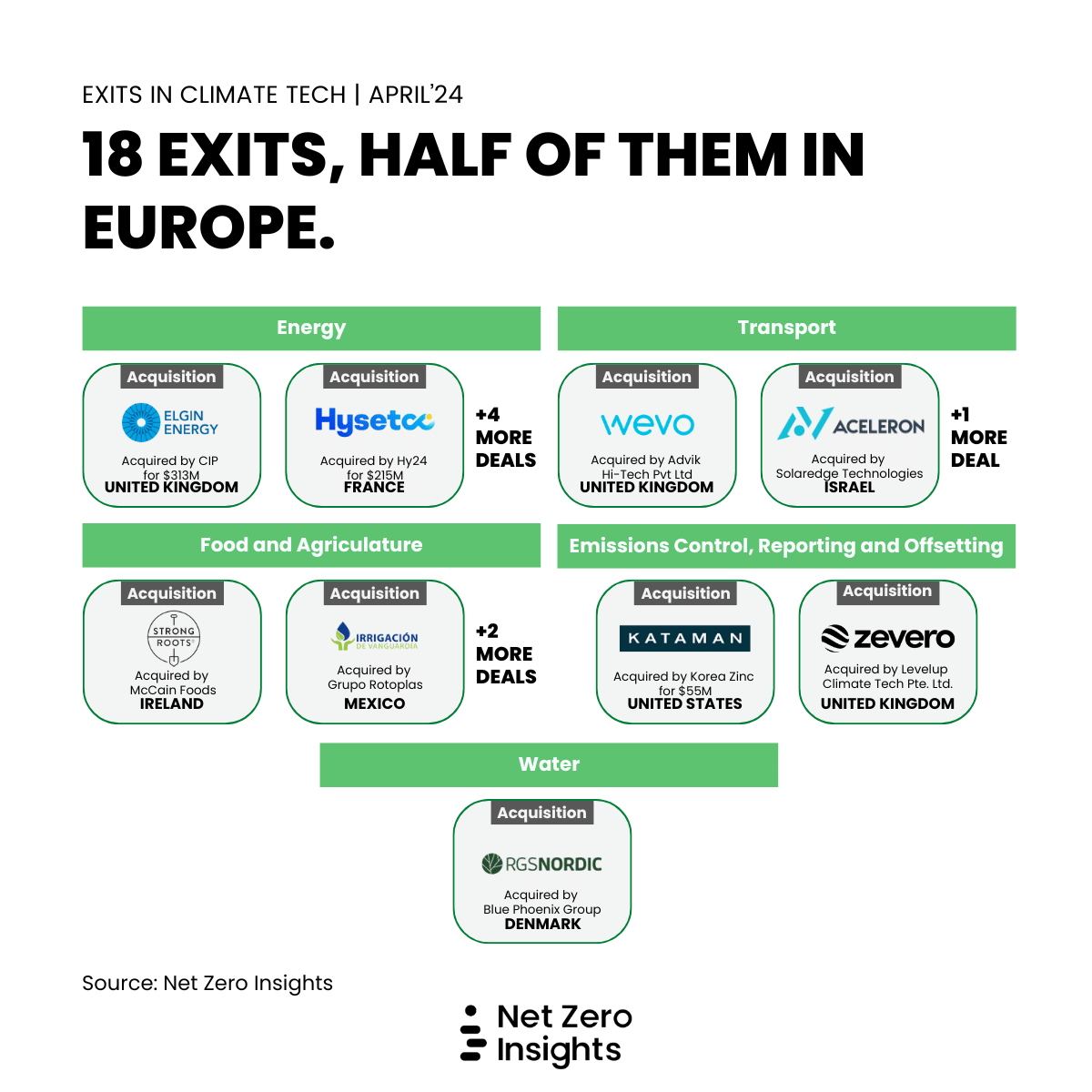

Climate tech exits: A for acquisitions

In the last 30 days, climate tech saw a noticeable uptick in exit activity, marked by a notable $632m in exit funding spread across 18 deals. What’s more all of these exits were acquisitions, reinforcing trends of a robust appetite for mergers and acquisitions within the venture ecosystem.

Furthermore, the exits that occurred within the month of April were dominated by corporations – 67% of all acquirers were corporate entities with aligned, strategic interests in the companies being acquired.

Out of the 18 exits observed in the past month, half took place in Europe, while the rest were distributed between North America and one deal in Israel. Energy, Transport, and Food & Ag. were the top three exited challenge areas, with these three deals comprising over 70% of exits.

The flurry of acquisitions in April hints at several underlying trends shaping the venture ecosystem within climate tech. For one, it reflects the growing interest from established companies in acquiring innovative startups as a means of staying ahead of the curve and tapping into new markets or technologies. Additionally, it underscores the attractiveness of startups as acquisition targets, particularly those with disruptive business models or proprietary technologies that can offer significant value to acquirers.